Singtel H2 net profit down 20.9% at S$2.2 billion; telco open to Aussie minority partner in Optus

Underlying earnings are up 10.6% at S$1.4 billion; record annual dividend of S$0.185 a share proposed

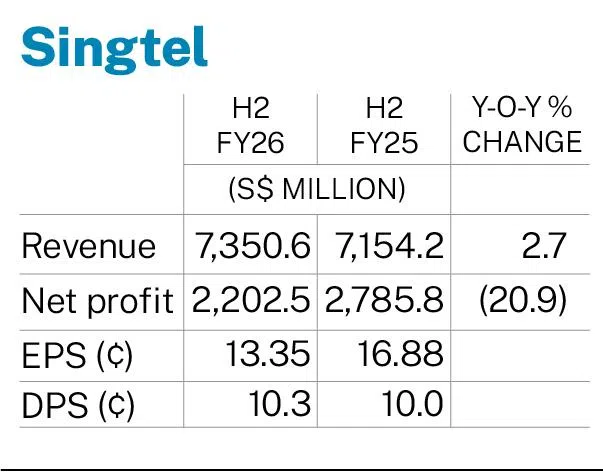

[SINGAPORE] Singtel on Thursday (May 21) posted a net profit of S$2.2 billion for its second half ended Mar 31, down 20.9 per cent from S$2.8 billion for the year-ago period.

This translated to earnings per share (EPS) of S$0.1335, down from S$0.1688 a year earlier.

The counter fell as much as 7.4 per cent or S$0.37 to S$4.65 in intraday trade. It closed 6.4 per cent or S$0.32 lower at S$4.70, with 118.1 million shares changing hands.

The telco said at an earnings briefing that the fall in its H2 earnings was due mainly to lower exceptional gains from its Indian associate, Airtel.

Excluding exceptional items, the group’s underlying net profit rose 10.6 per cent to S$1.4 billion from S$1.3 billion a year earlier.

Operating expenses rose to S$5.6 billion from S$5.4 billion, mainly due to investments in compliance and network resilience.

Navigate Asia in

a new global order

Get the insights delivered to your inbox.

Net finance expenses increased 16.6 per cent to S$195 million from S$167 million, on the back of foreign-exchange and fair-value losses.

H2 revenue came in at S$7.4 billion, up 2.7 per cent year on year from S$7.2 billion.

The board proposed a final ordinary dividend of S$0.103 per share, totalling S$1.7 billion for the financial year ended Mar 31. This consists of a core dividend of S$0.07 a share and a value realisation dividend of S$0.033 a share.

This brings Singtel’s total annual dividend to a record S$0.185 a share.

Full-year results

For FY2026, the group’s net profit rose 39.5 per cent to S$5.6 billion from S$4 billion in 2025.

This was boosted by a S$2.84 billion net exceptional gain, mainly from Airtel stake sales, and partly offset by various provisions largely from Australia.

Singtel’s underlying net profit climbed 12.1 per cent year on year to S$2.8 billion from S$2.5 billion, driven by growth in its regional associates Airtel and AIS, as well as operating companies NCS, Digital InfraCo and Optus.

Its full-year EPS stood at S$0.3398, up from S$0.2434 for the previous financial year.

Revenue was largely stable, up 0.8 per cent at S$14.3 billion, from S$14.1 billion previously.

In FY2026, Singtel undertook strategic and capital management initiatives aligned with its Singtel28 objectives. These aim to position the group to develop new revenue levers, pursue new growth opportunities as well as improve its capital efficiency.

These include its purchase of ST Telemedia Global Data Centres with KKR to accelerate its digital infrastructure strategy, asset recycling that has generated S$3.9 billion, and the Singtel special discounted share transfer exercise to improve its flexibility.

In a separate statement on Thursday, Singtel said it is open to an Australian partner taking a minority stake in Optus.

Miniority shareholders of Singtel, which fully owns Optus, have been concerned over its investment in the beleaguered Australian telco, given the emergency call outage last year which resulted in fatalities.

In a media briefing in November 2025, Singtel group CEO Yuen Kuan Moon noted that it had invested A$9 billion (S$7.7 billion) in capital expenditures at Optus over the past five years.

FY2027 outlook

Singtel plans to continue executing its Singtel28 strategy to grow its digital infrastructure and services. It is also repositioning itself as a global data centre player with some 2.8 gigawatts in design capacity.

It noted that Nxera’s 58 megawatt DC Tuas facility is almost fully contracted and “strong take-up” across its regional data centres.

Its digital services arm, NCS, is focusing on artificial intelligence acceleration across public sector, defence, homeland security, healthcare, transportation, telco and financial services.

Its near-term outlook for FY2027 is “more cautious” due to Middle East uncertainty, with earnings before interest and taxes growth forecast to be between low and mid-single digits.

With no operations in the Middle East, the group said its direct exposure to the region’s crisis is limited. However, it noted that most of its key markets are net energy importers and “susceptible to global energy price volatility”.

“While existing long-term power contracts should help mitigate this exposure, there could be second-order implications in the form of inflationary pressure resulting in higher operating costs, softer consumer and business spending and slower economic growth,” said Singtel.

“This will affect the group’s foreign-exchange risk stemming from volatility in the regional currencies where it operates, further impacting translated earnings.”

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.

TRENDING NOW

Haidilao co-founder’s family buys second bungalow in Cluny Hill for S$85 million

From hawker stall to Enterprise Award winner: How Han Keen Juan scaled the Old Chang Kee empire

Ban on land sales, new launches for developers that deliver ‘defect-ridden’ projects

Xi Jinping has just rewritten the rules of US-China rivalry