|

|

|

|

|

|

| FRI, FEB 27, 2026 | |

Kenneth Lim

Columnist

|

|

This week in ESG |

|

Sustainable finance |

OCBC under pressure for coal-financing disclosures |

|

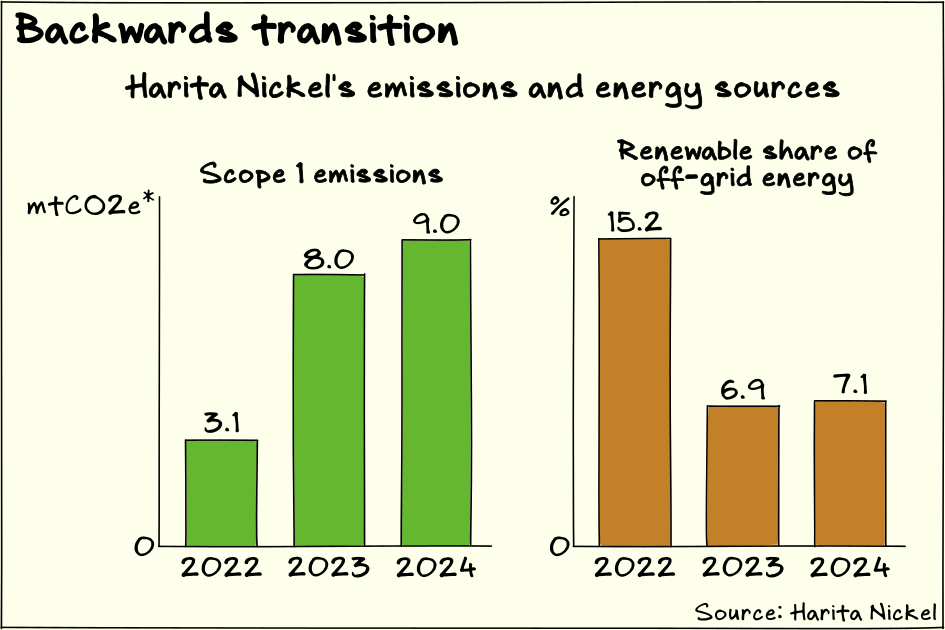

OCBC is the target in a complaint lodged with Singapore Exchange alleging inadequate disclosure by the Singapore lender on its exposure to coal. The complaint is the latest salvo by environmental group Market Forces, which had previously identified OCBC and its Singapore peers UOB and DBS as financiers for Indonesian miner Harita Nickel, whose facilities rely largely on coal for energy. The complaint alleges a “material information gap” between OCBC’s publicly stated sustainability commitments and the details of its financing for clients that are reliant on “captive coal”, which refers to off-grid coal-fired power. Market Forces argues that there are two material gaps in OCBC’s public disclosures on coal. The first stems from OCBC’s public commitments to cease project financing for new coal-fired power plants and corporate financing for clients where power generation capacity or revenue exceeds 25 per cent for new clients and 50 per cent for existing clients. However, Market Forces states that Harita Nickel’s power capacity at its facilities are primarily from captive coal plants. Market Forces also asserts that OCBC has not disclosed whether and how the bank’s coal-related metrics incorporate captive coal. OCBC group chief sustainability officer Mike Ng told The Business Times: “We are guided by our responsible financing framework and policies which outline our approach and dedication to managing (environmental, social and governance) risks within our lending practices, to ensure that our financial services do not adversely impact people, communities or the environment.” Without going into its merits, the existence of the complaint highlights a few lessons that South-east Asia’s listed companies should heed. The first is that it’s getting harder to greenwash. This is not a suggestion that OCBC is greenwashing, but an observation of an evolution in the market. As the new complaint shows, the market is becoming more sophisticated in how it scrutinises companies’ sustainability policies and disclosures, and more willing to take action when discrepancies are perceived. Like many developing markets, South-east Asia faces complex decarbonisation challenges. These include heavy reliance on coal and other fossil fuels, as well as significant social needs that must be balanced against the costs of climate action. Those complexities afford companies in the region some flexibility in the pace and scope of their climate strategies, but increasingly companies must be prepared to justify their choices. Naturally, the second lesson for companies is that credibility matters even more in this market environment. In the context of sustainability disclosures, credibility means that setting and complying with policies and targets must be sincere and transparent. Sincerity means that if a company claims that climate change is a material risk for the business, it needs to adequately address that risk. That includes ensuring that it has appropriate transition and mitigation strategies for all business segments with significant exposure, not just for segments that are convenient. If the company puts in place some climate policy or framework, it needs to abide by the spirit of the rules, because a breach means that the company isn’t managing risk properly. Market players have learnt to discern between companies that only set lofty climate goals and those that will get there. Transparency means giving stakeholders the means to understand climate policies and targets, and progress towards those policies and targets. Good disclosure helps to prevent misunderstandings. Honest discussions about progress build trust. Inadequate and unbalanced disclosures raise the risk of accusations about dishonesty, even if those accusations are wrong. The third lesson is that companies need to be serious about stakeholder engagement, which is a fundamental aspect of sustainability reporting. One of the biggest benefits of casting the net wide and then diving deep with stakeholders is that it reduces the risk of blind spots. A company could perhaps find out if an advocacy group thinks its climate policy is inadequate before that group tells everyone else. The fact is that Harita Nickel is a problematic climate citizen. Market Forces previously estimated that the miner was using about 890 megawatts (MW) of coal-fired power plants with an additional 1.2 gigawatts (GW) under construction. Total planned power supply comprised 2.54 GW from 25 coal plants and 1.3 GW from solar. Harita’s 2030 goal of 30 per cent reduction in greenhouse gas emissions is severely inadequate, since it doesn’t apply to facilities built after 2022; the company says baselines for facilities built after 2022 will be defined when they reach full operational capacity. Between 2022 and 2024, Harita’s coal energy consumption almost tripled from 22.9 gigajoules (GJ) to 60.1 million GJ. Renewable energy consumption growth only grew 56 per cent to 6.9 million GJ over the same period. Harita’s 2024 emissions of 10.9 million tonnes of carbon dioxide equivalent (mtCO2e) is 2.9 times what it was in 2022. Whether OCBC likes it or not, it is now in a position where it has to address Market Forces’ allegations. Investors – especially those with climate-related mandates – may need better explanations of how financing for Harita Nickel can be reconciled with the bank’s coal policies. There could also be questions about the credibility of Harita’s decarbonisation strategy, and how that might fit with OCBC’s transition financing framework. Nickel is an important component of batteries and financing nickel mining helps to support the energy transition, but that does not translate into a do-as-you-please pass. There should be a credible plan to transition Harita towards lower-carbon energy sources or to eventually sunset the financing if there is insufficient progress. OCBC may need to assure investors that it is not financing a coal-burning mine without a credible transition strategy. As Singapore’s banks grow their transition finance business, they will increasingly face scrutiny about their deals. That is rightly so, because transition finance is an area of sustainable financing that could easily be abused without proper safeguards. But that is all the more reason for the banks to strengthen their climate financing policies and targets, and to improve their disclosures. The more challenging it is to do something, the greater the reward for doing it well. |

Sustainable finance |

Looking beyond green financing |

|

Two deals by Parkway Life Real Estate Investment Trust (Reit) reflect growing sophistication in the regional sustainable finance market. The healthcare-focused Reit has obtained an 8.8 billion yen (S$72 million) 10-year social loan from DBS to refinance an existing loan to acquire nursing homes in Japan. This is the first social loan by DBS for the healthcare sector. Parkway Life Reit has also priced a S$70 million five-year green bond at a 2.103 per cent coupon to term out a loan for upgrading Mount Elizabeth Hospital to achieve Green Mark Platinum certification from Singapore’s Building and Construction Authority. UOB is the manager for the green bond. The two pieces of debt fall under the category of use-of-proceeds sustainable finance, where proceeds must be used for qualifying activities. Proceeds from social bonds must be used to advance social goals, while proceeds from green bonds must go towards environmental purposes. The new debt will relieve Parkway Life Reit of refinancing needs until March 2027, and will extend its weighted average debt maturity to 4.1 years from three years. Sustainable financing in South-east Asia has been gradually progressing beyond green use-of-proceeds debt. While total sustainable debt issuance in the region was largely flat at about US$63 billion in 2025, the volume of new social bonds rose more than 75 per cent to US$1.8 billion. Issuance of sustainability bonds, which can be used to finance both social and green activities, grew almost 35 per cent to US$9.8 billion. That growth suggests that companies and lenders are increasingly considering the use of sustainable financing for various activities, and that it’s becoming easier for various sustainable activities to obtain funding. This makes it easier for companies to invest more in sustainability. Lenders will also find the market more interesting. More avenues for raising sustainable funding enlarges the universe of companies that could potentially access sustainable finance. While some companies might need to borrow for environmental purposes, some might only want to do so for social objectives. The money is good, in more than one sense of the word. |

|

Did you receive this newsletter from someone? Sign up here to get the latest updates sent right to your inbox. |

|

|

|||||||||||||||||

|

|

|||||

|

|||||

|